Nigeria’s betting market doesn’t do things quietly. It never really has. Walk through any major city — Lagos, Abuja, Port Harcourt — and you’ll pass betting shops wedged between phone repair stalls and suya spots, screens flickering with Premier League odds while a dozen young men crowd the counter. That image hasn’t disappeared, but it’s been quietly displaced. The action has largely moved to the palm of the hand, powered by a fintech infrastructure that didn’t exist a decade ago and a regulatory system still, frankly, catching up.

A Market Built on Football and Mobile Phones

The Numbers Behind the Boom

The scale of what has been built here is genuinely striking. Sports betting accounts for around 75% of all wagers, with the English Premier League drawing the heaviest traffic, followed closely by local league fixtures. The online gambling market — combining sports betting, casino games, and virtual sports — was valued at approximately $641 million in 2024 and is widely projected to surpass $500 million in active revenue by the close of 2025. By 2029, some analysts put the ceiling at nearly $862 million.

Perhaps the most revealing statistic: over 60 million Nigerian adults — roughly 42% of the online population — are estimated to gamble online regularly. Nearly 90% of those bets are placed via mobile device. This is not a niche segment. It is a mass-market behaviour.

The Fintech Layer That Made It All Possible

If the smartphone opened the door, fintech walked through it. For most of the 2010s, the absence of reliable local payment gateways was the single biggest friction point for online betting in Nigeria. Many operators ran hybrid models — letting customers deposit cash at physical shops or through agents, with funds remitted centrally at the end of the day. That model worked, but it was slow, geographically limited, and excluded anyone outside a major urban centre.

The emergence of homegrown platforms like Flutterwave, Paystack, OPay, and PalmPay changed that equation entirely. A detailed investigation into how fintech now powers Nigeria’s gambling boom found that virtually every major bookmaker has integrated at least three of these payment rails simultaneously — a level of redundancy that keeps transactions flowing even when one provider experiences downtime.

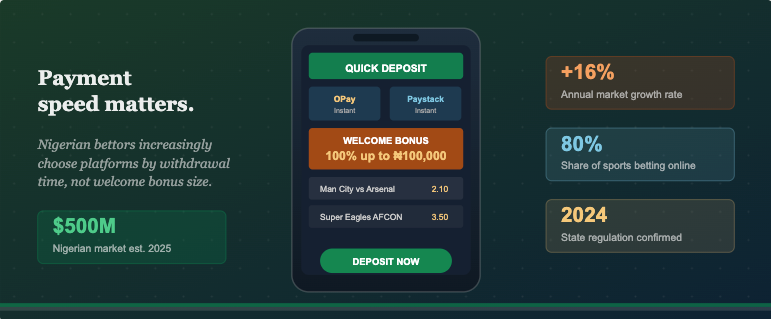

Show Image OPay and similar platforms have put instant digital payments within reach of tens of millions of Nigerians, including bettors in rural and semi-urban areas.

How the Payment Stack Works in Practice

Today, the majority of the best betting sites in Nigeria — including Bet9ja, SportyBet, 1xBet, BetKing, and Betano — integrate multiple local payment rails simultaneously. A bettor can fund their account via a Paystack card gateway, a Flutterwave bank transfer, an OPay mobile wallet, or a Monnify virtual account. All of these channels sit on top of Nigeria’s NIBSS Instant Payment (NIP) system, which processes transfers in real time and handles billions of naira in daily volume across the entire economy.

OPay alone reported that its betting platform partners processed over one million transactions in Q1 2025, with an average deposit of just ₦1,500 — roughly $1. That micro-transaction threshold matters enormously. It means that bettors with limited disposable income, who would never have engaged with the older cash-agent system, can now participate from wherever they are with whatever they have. For operators, it broadens the addressable market. For fintechs, every bet placed is a transaction fee earned.

| Payment Method | Deposit Limit (typical) | Withdrawal Limit | Speed | Key Bookmakers |

| Flutterwave | Up to ₦500,000 | Up to ₦9,999,999 | Instant | Bet9ja, Betway, 1xBet |

| Paystack | Up to ₦500,000 | Varies by operator | Instant | NairaBET, Betano, BetKing |

| OPay | Up to ₦300,000 | Up to ₦500,000 | Instant | Bet9ja, 22Bet, SportyBet |

| Bank Transfer (NIP) | Unlimited | Unlimited | Instant | All major operators |

| PalmPay | Up to ₦200,000 | Up to ₦500,000 | Instant | BetKing, 22Bet |

Table 1 — Overview of key payment methods used by Nigerian bettors as of mid-2025. Limits and availability vary by operator and can change following CBN policy updates. Data compiled from operator deposit pages and platform documentation.

A Regulatory Landscape in Transition

The legal backdrop to all of this has shifted considerably, and not in a linear direction. For most of the past two decades, Nigeria’s gambling sector was nominally governed at the federal level by the National Lottery Regulatory Commission (NLRC), created under the National Lottery Act of 2005. States like Lagos operated parallel frameworks through bodies like the Lagos State Lotteries and Gaming Authority (LSLGA), creating a dual-licensing requirement that added cost and complexity for operators.

Then came November 2024. In a landmark ruling, Nigeria’s Supreme Court struck down the National Lottery Act entirely, holding that lotteries and games of chance fall outside federal legislative authority. Regulatory power over gambling is now constitutionally vested in individual state governments — with the NLRC retaining jurisdiction only within the Federal Capital Territory. Overnight, every operator with a national licence found themselves navigating a patchwork of 36 state frameworks. Reporting from December 2025 described the situation bluntly: the sector had gone from regulatory complexity to outright legal limbo almost overnight.

A Central Gaming Bill (HB 2062), sponsored by Deputy Speaker Benjamin Kalu and aimed at harmonising the system, cleared its third reading in the Senate in 2025, but legal experts have flagged potential constitutional obstacles. Until that bill passes and is tested, the regulatory grey area persists.

On the payment side, the CBN has tightened its grip on fintech considerably. In 2024 and 2025, it fined Paystack for operating an unlicensed wallet product and temporarily froze new user onboarding at OPay and Moniepoint over anti-money laundering concerns — actions not specifically directed at gambling, but which demonstrate that the payment rails underpinning the sector are under greater scrutiny than before. All operators are also now required to enforce Know Your Customer (KYC) checks as part of their account-opening and withdrawal flows, linking identity verification directly to AML compliance. A new cybercrime levy of 0.005% on all electronic transactions is also now in effect under the Cybercrime (Prohibition, Prevention, etc.) Act.

The coming Nigerian Tax Act (NTA) 2025, set to take effect from January 2026, will fold gaming companies into the mainstream tax framework, ending their treatment under the separate lottery tax regime that had applied a 7% rate on net proceeds.

| Regulatory Milestone | Year | Impact on Sector |

| National Lottery Act enacted | 2005 | Federal licensing framework established |

| Lagos State Gaming Authority active | 2007 | Parallel state-level licensing introduced |

| CBN fintech KYC mandates tightened | 2024 | Stricter identity verification for all operators |

| Supreme Court nullifies National Lottery Act | Nov 2024 | Licensing power devolved to individual states |

| WHT on player winnings introduced | 2024 | New tax burden on withdrawals |

| Central Gaming Bill (HB 2062) passes Senate | 2025 | National harmonisation attempt, outcome pending |

| Nigerian Tax Act 2025 enacted | 2025 | Gaming firms enter standard corporate tax regime from 2026 |

Table 2 — Key regulatory milestones shaping Nigeria’s online betting and payments landscape. The pace of change since 2024 reflects both a maturing market and sustained government pressure to formalise it.

What It Means for Bettors on the Ground

For the average Nigerian bettor, the day-to-day experience has genuinely improved — deposits land in seconds, withdrawals process in minutes rather than days, and the range of platforms has expanded considerably. The integration of USSD codes means that even users without smartphones or reliable data access can place bets and check balances using a basic feature phone.

The friction that remains is largely regulatory. The post-November 2024 landscape means operators are, in some cases, uncertain about which licences they need and in which states. There have been reports of temporary suspensions and access issues as platforms scramble to comply with new state-level requirements. For bettors, this occasionally manifests as unexpected site downtime or restricted account functionality in certain regions.

For those navigating alternative payment options — including emerging tools like crypto wallets, stablecoins, and the recently launched cNGN naira-pegged stablecoin — it’s worth understanding how these instruments interact with local AML rules. A useful primer on how cryptocurrency is being adopted across African markets offers context for where Nigeria fits within a broader continental trajectory.

Conclusion: Infrastructure First, Regulation Catching Up

Nigeria’s online betting sector is, structurally, one of the most sophisticated on the African continent. The fintech infrastructure is deep, competitive, and increasingly capable of handling micro-transactions at scale — a combination that mirrors what drove mobile money adoption across East Africa but applied to a gambling use case. The market’s trajectory toward $862 million by 2029 is plausible, assuming the regulatory environment doesn’t create sustained operational disruption.

The real uncertainty sits at the intersection of state-level fragmentation and federal ambition. The Central Gaming Bill, if enacted in a constitutionally durable form, could deliver the clarity that both operators and investors need. Until then, Nigeria’s betting sector will continue to do what it has always done: move fast, adapt, and find a way through.

The next three years will likely determine whether Nigeria becomes the definitional model for regulated mobile betting in Africa — or a cautionary tale about what happens when infrastructure outpaces governance.